What Happens When You Hire an Insolvency Practitioner Many UK directors and business owners face stressful financial problems—ranging from mounting debts to the risk of compulsory liquidation. When these challenges surface, seeking professional support can be the turning point. Hiring an insolvency practitioner UK for your company brings legal protection, business rescue opportunities in the […]

Is Insolvency the Same as Liquidation? Understanding the Difference

November 20, 2024

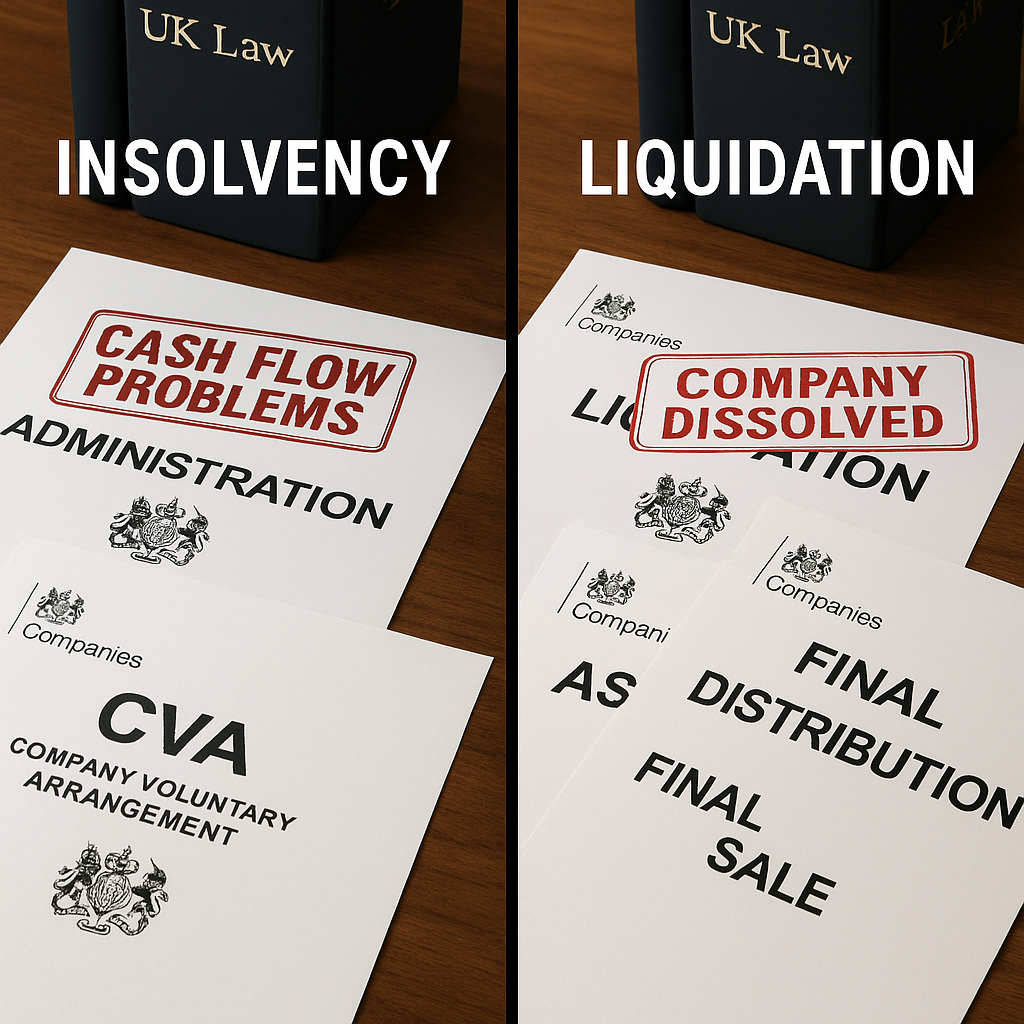

Business owners and company directors often face the challenging question: is insolvency the same as liquidation? This confusion can add stress during financial difficulties. Understanding this difference plays a crucial role in making informed decisions about your company's future. Insolvency is a financial state where a company cannot pay its debts when they fall due, whilst liquidation is the formal process of closing down a business and distributing its assets to creditors. Our guide will take you through each concept, clarifying their roles, processes, and effects on your business. We'll also explore the insolvent liquidation process, explaining how it works when a company is unable to meet its financial obligations and the steps taken to wind up the business. Insolvency occurs when a company cannot meet its debts as they fall due. This financial state can lead to severe consequences, including the risk of entering formal insolvency procedures under the Insolvency Act 1986. An insolvent company may face legal actions from creditors, and directors might be subject to restrictions or disqualifications. Insolvency indicates a critical situation where immediate action is necessary to either rescue the business through restructuring or consider liquidation to repay liabilities. An insolvency practitioner plays a crucial role in handling the affairs of an insolvent company. This professional assesses the company's financial position and guides the directors on suitable measures, such as proposing a Company Voluntary Arrangement (CVA), entering administration, or preparing for liquidation. Their goal is to achieve the best outcome for all parties involved, minimising negative impacts on creditors, employees, and shareholders alike. Engaging with an experienced insolvency practitioner early can substantially increase the chances of recovery or orderly wind-down. Insolvency refers to a financial state where a company or individual cannot pay their debts as they fall due. This situation indicates financial distress and may lead to various legal consequences under insolvency law. A business facing cash flow problems or balance sheet issues finds itself unable to meet its liabilities, signalling insolvency. This condition is the first step that might eventually lead to liquidation if unresolved. It's crucial for company directors and business owners to recognise this status early on, as it can affect the ability to continue operations. Under the Insolvency Act 1986, there are two tests for insolvency: the cash flow test (inability to pay debts as they fall due) and the balance sheet test (liabilities exceeding assets). Insolvency law outlines procedures for dealing with insolvent companies, including potential recovery avenues through administration or voluntary arrangements. Insolvency practitioners play a crucial role in advising and guiding businesses through these difficult times. Their expertise helps determine whether a company can recover or should enter liquidation – winding up the affairs of an insolvent firm by selling off assets to pay creditors. Recognising the signs of insolvency early provides more options for resolution, potentially avoiding compulsory liquidation by court order. After defining insolvency, it becomes crucial to identify the signs that a company is becoming insolvent. Recognising these indicators early can prevent further financial deterioration. The company is unable to pay debts as they fall due, indicating cash flow problems. Legal actions commence against the company for unpaid debts, showcasing creditor pressure. A company's liabilities exceed its assets on the balance sheet; this is known as balance sheet insolvency. Suppliers put the company on cash-on-delivery (COD) terms because of late payments. The company issues warnings to shareholders about potential liquidity problems. Directors use personal funds to keep the business afloat, highlighting acute financial distress. Employees experience delayed salary payments, reflecting cash management issues. The company faces a withdrawal of credit facilities by banks or suppliers, tightening liquidity further. Frequent changes of accountants or auditors might signal attempts to find favourable financial interpretations. Increased borrowing reaches levels that are unsustainable for operational cash flow needs. Each sign on its own may not mean a company is insolvent, but when multiple signs appear together, it strongly suggests financial instability needing immediate attention from an insolvency practitioner to assess and advise on viable restructuring or liquidation options. Once signs of insolvency emerge, a licensed insolvency practitioner plays a critical role. This professional steps in to manage the situation efficiently. Their foremost duty involves assessing the company's financial health objectively. They decide whether restructuring, entering into administration, or pursuing a Company Voluntary Arrangement may salvage the business or if liquidation is inevitable. Insolvency practitioners are regulated by recognised professional bodies including the Institute of Chartered Accountants in England and Wales (ICAEW). An insolvency practitioner takes control of the company during this challenging period. They work diligently to pay off debts, often negotiating with creditors for more favourable terms or payment arrangements. If liquidation becomes necessary, they ensure an orderly process, aiming to maximise returns for all stakeholders involved whilst complying with their statutory duties under the Insolvency Act 1986. Liquidation marks the end of a company's life by selling its assets to pay off debts. The liquidator takes control of this process under the provisions of the Insolvency Act 1986. They sell everything the company owns, from property to inventory and intellectual property. Money from sales goes first to secured creditors, then to preferential creditors (including employees for certain claims), and finally to unsecured creditors. If anything remains after paying all creditors, it may be distributed to shareholders. There are different types of liquidation available: voluntary and compulsory. In voluntary liquidation, directors or members decide to close their business through either a Members' Voluntary Liquidation (MVL) for solvent companies or a Creditors' Voluntary Liquidation (CVL) for insolvent companies. Compulsory liquidation happens when creditors force the company into this situation through a court order. Both scenarios involve a licensed insolvency practitioner appointed as a liquidator to manage the dissolution of the company. Companies face different routes for liquidation: compulsory and voluntary. Compulsory liquidation happens when a court orders the dissolution of a company, typically after creditors file a winding-up petition because the company cannot pay its debts. This is often seen as the last resort when other options have been exhausted. The Official Receiver initially acts as liquidator before a licensed insolvency practitioner may be appointed. On the other hand, voluntary liquidation occurs when the directors of a solvent or insolvent company decide to stop business operations. This provides more control over the process and timing. Understanding whether to pursue Members' Voluntary Liquidation (MVL) or Creditors' Voluntary Liquidation (CVL) hinges on one critical factor - solvency. The directors must make this determination based on their assessment of the company's ability to pay its debts in full within 12 months. Members' Voluntary Liquidation applies to companies that are still solvent but choose to dissolve for strategic reasons. It allows them to distribute assets amongst members after settling all debts, often providing tax advantages for shareholders. Conversely, Creditors' Voluntary Liquidation pertains to those unable to meet financial obligations, giving control over asset distribution primarily to creditors rather than shareholders or directors. The process of liquidation starts by appointing a qualified insolvency practitioner to manage the company's liquidation. This individual gains authority over the company with the goal to liquidate assets in a manner that optimises returns for creditors and, where applicable, shareholders. They evaluate the worth of the company's assets, which could include property, inventory, plant and machinery, and intellectual property. These assets are subsequently sold by the practitioner, converting them into cash through various methods. After the sale of assets, the generated funds are used to settle the company's liabilities. Payment is provided to creditors according to the statutory order of priority defined by insolvency law, starting with the costs of liquidation, then secured creditors, preferential creditors, and finally unsecured creditors. If any funds remain after settling all liabilities, they are distributed amongst the shareholders according to their rights. Simultaneously, the liquidator takes care of legal aspects and submits required documents to Companies House. Upon finalising these tasks, they apply for the company to be dissolved and removed from the Companies House register, officially terminating the company's existence. Following an explanation of the liquidation process, it is crucial to understand what a liquidator does. A liquidator takes control of the company during its wind-up phase. Their primary duty is to collect and sell the company's assets for the benefit of creditors. They use the proceeds from these sales to pay company debts according to the statutory order of priority. This involves paying off secured creditors first, then preferential creditors, and finally unsecured creditors before distributing any remaining funds to shareholders. Liquidators must also investigate the company's financial affairs thoroughly. They look for transactions at an undervalue, preferences, or other recoverable transactions that occurred before liquidation. If they find any, they can take legal action to recover assets for the benefit of creditors. The liquidator also has a duty to investigate the conduct of directors and report any evidence of wrongful trading, fraudulent trading, or other misconduct to the Insolvency Service. Managing taxes owed by the company is another critical responsibility. Liquidators ensure that all tax matters are settled correctly, including VAT, corporation tax, PAYE, and National Insurance contributions. Insolvency is a financial state where a company cannot meet its debts as they fall due or where its liabilities exceed its assets. This status doesn't always lead to closing the business. An insolvency practitioner steps in to assess whether the company can survive through restructuring, entering administration, or pursuing a Company Voluntary Arrangement. The process may involve negotiating with creditors and exploring various rescue mechanisms available before considering liquidation as a final option. Liquidation marks the end of a company's journey, initiated when recovery seems impossible or as part of an orderly shutdown via Members' Voluntary Liquidation (MVL) for solvent companies. A licensed insolvency practitioner transforms into a liquidator, taking control of all assets for selling and distributing funds amongst creditors and shareholders. Contrary to insolvency, which might offer a pathway to recovery through various procedures, liquidation finalises the closure and distribution of assets, leading to the company's dissolution. A company faces insolvency when it can't pay its debts on time or when its liabilities exceed its assets. This situation may lead to liquidation, but the two are not the same. Insolvency is a financial state of being unable to cover owed amounts, whilst liquidation refers to the process of closing down a company and distributing its assets to creditors. Liquidation might be voluntary or compulsory and may occur as an outcome of insolvency, but it can also happen to solvent companies for strategic reasons. Insolvency is about financial inability, whereas liquidation means ending the company's existence. The interaction between insolvency and administration reveals crucial paths for addressing financial difficulties without necessarily leading to liquidation. Understanding these differences helps directors decide how best to proceed during difficult times. A licensed insolvency practitioner's role becomes critical here; they guide companies through either recovery options or winding up processes based on their condition. Insolvency can lead to liquidation, marking a critical phase in a company's lifecycle. Insolvency occurs when a firm cannot pay its debts on time or when liabilities surpass assets under either the cash flow or balance sheet tests. This situation often prompts directors to seek advice from an insolvency practitioner. The practitioner assesses the company's viability and may recommend liquidation as the path forward if recovery seems unlikely through other means. During liquidation of an insolvent company, the assets get sold off to repay creditors according to the statutory order of priority. The appointed liquidator takes control, shutting down operations and distributing proceeds from asset sales according to legal requirements. Liquidation signifies the end of a business directly stemming from insolvency events. It ensures that creditors recover as much as possible whilst legally dissolving the company. Creditors face significant risks during insolvency and liquidation processes. They might not recover all the money owed to them, particularly unsecured creditors who rank lower in the statutory order of priority. This situation becomes more challenging if a company enters compulsory liquidation, as this method prioritises clearing secured debts and the costs of liquidation first. Unsecured creditors, such as suppliers or utility providers, often receive only a fraction of what they are due, if anything at all. The Insolvency Act 1986 sets out the order in which creditors are paid, with secured creditors having the best chance of recovery. Shareholders also find themselves in a difficult position when a company faces insolvency or decides to liquidate. In voluntary liquidation scenarios like Members' Voluntary Liquidation (MVL), shareholders may see some return from the distribution of assets after all debts have been settled. However, in situations where the company's liabilities exceed its assets, shareholders are likely to receive nothing, reflecting their position as the last in line for any form of financial distribution during the winding-up process. A company becomes insolvent when it cannot pay its debts as they fall due, known as cash flow insolvency. This state may also occur if the business's liabilities exceed its assets, indicating balance sheet insolvency under the tests established by the Insolvency Act 1986. Directors must assess their company's financial health to avoid trading whilst insolvent, which can lead to severe legal consequences including personal liability for wrongful trading. Determining if a company is unable to continue operations involves close examination of its cash flows and liabilities. If a company delays payments consistently or receives legal warnings from creditors, these are strong indicators of insolvency. A licensed insolvency practitioner should be consulted in such cases to review the situation and recommend a course of action, potentially including liquidation, administration, or a Company Voluntary Arrangement. Recognising when a company is unable to fulfil its debts is vital for business proprietors, company directors, and financial professionals. Understanding the early symptoms can prevent further financial harm and potential director liability. Frequent delays in paying creditors highlight a company's struggle with cash flow, hinting at possible insolvency. Creditors send formal demands for payment, such as statutory demands, signifying severe liquidity problems. The company faces overdraft limits being consistently hit or exceeded, demonstrating dependence on bank support without sufficient incoming revenues. Legal proceedings initiated against the company for nonpayment of debts demonstrate a failure to fulfil financial obligations. Suppliers commence demanding cash on delivery (COD), rejecting credit terms due to previous payment failures. Business leaders implement personal assets to support the enterprise; this is generally a desperate measure signifying intense financial distress. The rapid decline in cash reserves without matching revenue generation emphasises unhealthy financial conditions. Regular adverse commentary from balance sheet evaluations where liabilities exceed assets indicates insolvency risk. The difficulty of paying staff wages punctually proves that the company's liquidity is weakened. Frequently requesting extensions on debt repayments displays an incapability to fulfil original contracts. These symptoms necessitate prompt consideration and action from management to address potential insolvency issues before considering liquidation as an alternative. Facing insolvency brings about significant legal consequences that can impact a company's future operations and its directors personally. Directors must be aware of their responsibilities to avoid wrongful trading, which can lead to personal liability for company debts. Upon declaring insolvency, the directors may lose control over the company's assets and affairs; these are then handed over to an appointed insolvency practitioner. This shift marks a critical change, as the practitioner aims to settle debts by selling off assets. Insolvency doesn't just threaten a company's survival; it fundamentally changes who has control and decision-making authority. Creditors too face repercussions during this period. They may receive only partial payments or sometimes none at all, depending on how the assets are distributed according to the statutory order of priority. Insolvency proceedings also open up the company's affairs for scrutiny; ensuring compliance with financial obligations becomes paramount for directors seeking to mitigate legal risks associated with insolvency and potential liquidation scenarios. Liquidation marks a crucial turning point for any company, indicating the termination of its business operations by selling off assets to settle debts. This process is primarily categorised into two types: compulsory and voluntary liquidation. In compulsory liquidation, a court mandates the dissolution of the company following a winding-up petition from creditors due to insolvent conditions. This form signifies a forced procedure where the company is unable to resolve its debts and the court intervenes. On the contrary, voluntary liquidation occurs when the directors or shareholders elect to shut down a solvent company (Members' Voluntary Liquidation - MVL) or an insolvent company (Creditors' Voluntary Liquidation - CVL). An MVL facilitates the distribution of surplus assets to shareholders after all debts have been cleared, indicating a financially sound winding-up with potential tax advantages. Conversely, CVL caters to instances where the company is incapable of meeting its liabilities, providing an orderly method for winding up under insolvency situations. Members' Voluntary Liquidation (MVL) is a form of liquidation for solvent companies. Directors must make a statutory declaration of solvency, confirming the company can pay its debts in full within 12 months of the commencement of winding up. This process allows shareholders to realise their assets efficiently and often provides significant tax advantages, particularly for capital gains tax and entrepreneurs' relief. An MVL often marks the end of a successful company's journey when it has served its purpose, the owners decide to retire, or there's a need to extract accumulated profits in a tax-efficient manner. The process is entirely voluntary and controlled by the shareholders. The role of an insolvency practitioner becomes crucial here, as they oversee the liquidation process ensuring all legal requirements are met. They work on distributing assets to shareholders after paying off any debts and dealing with all regulatory requirements. Initiation of Creditors' Voluntary Liquidation (CVL) occurs when company directors determine the business is unable to fulfil its debt liabilities and cannot make a declaration of solvency. Their course of action is to liquidate voluntarily, with the intention of settling as many debts as possible. A qualified insolvency practitioner is appointed to oversee this process. This involves evaluating the company's assets before selling them through the most appropriate method to maximise realisations. The proceeds from these sales are utilised to repay the company's creditors according to the statutory order of priority. In a CVL, priority is given to secured creditors, followed by preferential creditors including employees for certain claims such as wages and holiday pay. Remaining funds are distributed amongst unsecured creditors, such as suppliers or HM Revenue & Customs. By closely monitoring cash flow and the level of debts, this stage may be avoided through early intervention. Yet, if liquidation is unavoidable, prompt action through CVL can help limit the impact for all parties involved. Understanding the distinctions between insolvency and liquidation is essential for business owners, company directors, and financial professionals. Insolvency represents a condition where a company is unable to pay its debts, possibly leading to various legal paths including administration, Company Voluntary Arrangements, or liquidation. Conversely, liquidation indicates the completion of a company's journey by selling off assets to pay creditors and ultimately dissolving the company. This distinction is crucial because it affects the decision-making processes and outcomes for all stakeholders involved. For those managing limited companies or handling financial strategies, understanding these differences ensures informed decisions are made during times of economic distress. The engagement of insolvency practitioners or liquidators might be essential to manage such situations effectively, underlining the significance of professional guidance in handling financial difficulties within businesses. Early recognition of financial problems and prompt professional advice can often provide more options for resolution, whether through rescue mechanisms or orderly liquidation procedures that maximise returns for creditors and minimise personal liability for directors.

What is Insolvency, and How Does it Affect a Company?

Definition of Insolvency

Signs a Company is Insolvent

Role of an Insolvency Practitioner

Exploring Liquidation: What Does it Mean?

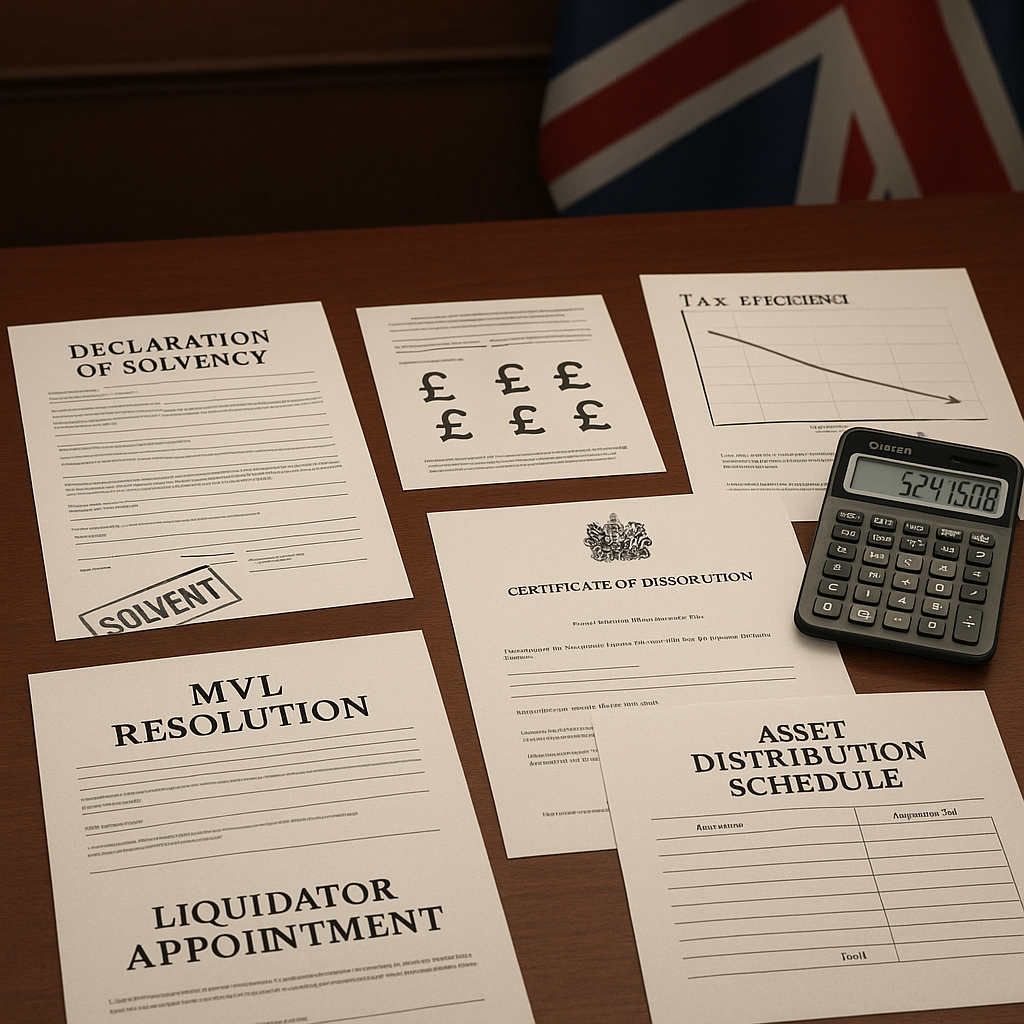

Different Types of Liquidation

The Liquidation Process Explained

Responsibilities of a Liquidator

Difference Between Insolvency and Liquidation: Key Concepts

Understanding the Key Differences

How Insolvency and Liquidation Interact

Implications for Creditors and Shareholders

When is a Company Insolvent?

Indicators that a Company Cannot Pay its Debts

Legal Consequences of Being Insolvent

What are the Different Types of Liquidation?

Exploring Members' Voluntary Liquidation (MVL)

Understanding Creditors' Voluntary Liquidation (CVL)

Conclusion

Recent Posts

How Are Insolvency Practitioners Appointed and What Is Their Role?

Read More

How Are Insolvency Practitioners Appointed – UK Expert Guide Navigating financial turmoil can be overwhelming for company directors and sole traders alike. Faced with mounting debts, threats of compulsory liquidation, or creditor demands, knowing “how insolvency practitioners are appointed” becomes crucial for preserving your organisation. In the UK, professional insolvency services, such as company voluntary […]

How an Insolvency Practitioner Helps with Company Administration

Read More

Administration might be your lifeline when your company's drowning in debt and creditors are circling. But here's what most directors don't understand: it's not just about buying time — it's about buying the right kind of time, with the proper professional support. The difference between administration working for you or against you often comes down […]

Can an Insolvency Practitioner Stop Creditors? Key Insights

Read More

Can an Insolvency Practitioner Stop Creditors? In the UK, mounting pressure from creditors can disrupt cash flow, increase stress for directors, and push a company toward insolvency. Professional guidance plays a pivotal role in countering these challenges. Nexus Corporate Solutions Limited specialises in helping businesses find relief from persistent creditors, providing strategic solutions that align […]

How Insolvency Practitioners Manage Company Assets in the UK

Read More

When your company's in financial trouble, one of the biggest worries is what happens to everything you've built. Your equipment, property, stock — the assets that represent years of hard work. It's a valid concern, and you're not alone. The reality? How insolvency practitioners handle your company's assets can make or break the outcome for […]

Insolvent Trading Penalties: Key Facts for UK Directors

Read More

Insolvent trading can trigger severe repercussions for UK directors, including personal liability and possible disqualification. When a business is unable to pay debts and continues to trade without a reasonable prospect of avoiding insolvency, the law may classify this as wrongful trading. The Insolvency Act 1986, alongside related legislation, outlines civil and criminal penalties for […]

Signs of Business Insolvency: What UK Directors Need to Know

Read More

Recognising the signs of business insolvency early is vital for UK companies. Overlooked warning signals—such as recurring cash flow issues, unpaid HMRC tax arrears, or missed staff wages—can quickly escalate into serious risks that demand immediate attention. Being aware of these common signs of business insolvency enables directors to take timely action, whether through careful […]

Impact of Insolvency on Suppliers: Protecting Your UK Business

Read More

Supplier insolvency can have serious consequences for UK companies, creating ripple effects that extend beyond the affected supplier. Cash flow interruptions, delayed payments, and increased operational risks are common outcomes. When a key supplier or client becomes insolvent, contracts may be disrupted, insurance coverage can be affected, and overall profitability may decline. Nexus Corporate Solutions […]

Struggling with IVA Monthly Payments: UK Debt Solutions

Read More

Struggling with IVA monthly payments can feel overwhelming, especially when daily financial obligations pile up. An Individual Voluntary Arrangement (IVA) is designed to help those in debt regain stability by consolidating and managing repayments under a legally binding agreement. However, life changes—like reduced monthly income, sudden expenses, or shifts in personal circumstances—often make sticking to […]

Problems Renting After IVA: Overcome Rental Challenges

Read More

Experiencing financial difficulty can make everyday life more challenging, especially when an individual or business director needs to secure a stable living arrangement. In the UK, an Individual Voluntary Arrangement (IVA) offers a legally binding debt solution that eases pressure from creditors. However, many worry about problems renting after IVA. Questions about how this might […]

Related Articles from the same category:

Company Registration Number: 14873516

Address: Apex Building, 1 Water Vole Way, Balby, Doncaster, South Yorkshire, DN4 5JP

Tel: 01302 430180

Address: Apex Building, 1 Water Vole Way, Balby, Doncaster, South Yorkshire, DN4 5JP

Tel: 01302 430180